Should You Convert Your IRA to a Roth?

Financial PlanningJun 17, 2026

If you’ve spent your career saving into a 401(k) or Traditional IRA, you’ve built up a big pile of money that’s never been taxed. That was the deal. Skip taxes now, pay them later when you withdraw.

A Roth conversion flips that deal. You pay the tax today on some (or all) of that money, move it to a Roth account, and from that point forward it potentially grows tax-free, and comes out tax-free when you need it.

Sounds great, right? Sometimes it is. Sometimes it’s a costly mistake. The difference comes down to a few key questions.

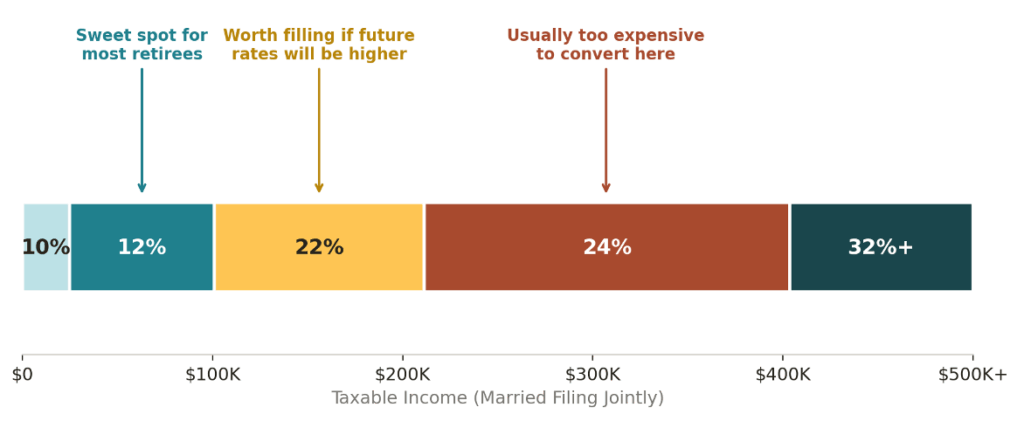

The Big Picture: Are You Paying Less Now Than You Will Later?

That’s the whole game in one sentence. If your tax rate today is lower than your tax rate will be in retirement (or your kids’ rate when they inherit), converting makes sense. If it’s higher, it usually doesn’t.

Here’s what 2026 tax brackets look like for a married couple and where conversions tend to make sense:

What to Think About Before You Convert

There’s no single right answer. Here are the questions we walk through with our clients:

- What’s your tax rate today vs. retirement? Working and earning a high salary? Probably a bad time. Retired with low income before Social Security starts? Probably a great time.

- Can you pay the tax from outside the IRA? Conversions work much better when you can pay the tax bill from a regular savings or brokerage account. Pulling extra from the IRA itself to cover taxes defeats much of the benefit.

- Will it push up your Medicare premiums? Once you’re 63 or older, conversion income can trigger higher Medicare Part B and D premiums two years later. We watch these thresholds carefully.

- Will it affect your Social Security taxes? Adding income can make more of your Social Security check taxable. There’s a sweet spot before benefits start when conversions are usually cheaper.

- What about Required Minimum Distributions? At age 73 (75 if you were born after 1960) the IRS forces you to start withdrawing from your Traditional IRA whether you need the money or not. A big balance means big forced withdrawals, and a big tax bill.

- Who inherits this money? If your kids inherit a Traditional IRA, they have 10 years to drain it, often during their highest-earning years. Inheriting a Roth means tax-free money for them.

- Are you charitably inclined? If you plan to give money to charity in retirement, leaving funds in the Traditional IRA may be smarter. Charities don’t pay tax on what they receive.

- How long until you need the money? The longer the converted dollars get to grow tax-free, the better the math works. Conversions reward patience.

Three Real-World Stories

Let’s look at three couples in different situations. The names are made up, the math isn’t.

Case Study 1: Tom & Linda – A Textbook Win

Both 63. Just retired. Living in Pennsylvania.

| Traditional IRA | $1.6 million combined |

| Brokerage account | $450,000 (available for tax payment) |

| Pension | $32,000/year |

| Social Security | Not yet (delaying to age 70) |

| This year’s income | Very low (just the pension) |

The opportunity:

Tom and Linda have a 7-year window between retirement and the start of Social Security where their income is unusually low. After that, Social Security kicks in, and at age 75 the IRS will start forcing them to take big withdrawals from that $1.6M IRA, which by then could be $3 million or more.

If they do nothing, those forced withdrawals will land them squarely in the 22–24% federal tax bracket for the rest of their lives. Their kids would then inherit the rest and have to drain it within 10 years, likely during their own peak earning years.

The move:

Convert about $100,000 from the Traditional IRA to a Roth this year. That fills up their 12% tax bracket exactly, they don’t spill into 22%. Federal tax cost: roughly $11,500, or about 11% blended. Pennsylvania doesn’t tax retirement withdrawals after 59½, so there’s no state tax. They pay the federal tax from the brokerage account, so 100% of the $100K keeps growing in the Roth.

Then they repeat this for about 7 years. By the time RMDs kick in, they’ve shifted around $700,000–$800,000 to the tax-free side of the ledger at a blended rate near 11%, instead of paying 22–24% on it later.

Why this works:

Low current income + cash to pay the tax + long runway + no state tax + heirs in hight brackets = textbook good fit.

Case Study 2: Dr. Patel – A Costly Mistake Avoided

Age 58. Cardiologist. Living in New Jersey. Plans to retire at 67 and move to Florida.

| Salary | $620,000 |

| Spouse’s salary | $90,000 |

| 401(k) | $2.1 million |

| Current tax bracket | 32–35% federal + 10.75% NJ |

| Retirement plan | Move to Florida (no state income tax) |

| Charitable giving | Significant (plans large gifts in retirement) |

The pitch she received:

A salesperson told Dr. Patel she should convert $200,000 “before tax rates go up.” The pitch sounded urgent. The math, when we ran it, didn’t add up.

Why we said wait:

- She’s already in the 32–35% federal bracket. Stacking another $200K on top pushes the conversion into 35%.

- New Jersey would take another 10.75%, money she’ll never get back, because she’s moving to Florida in 9 years.

- She doesn’t have enough outside cash to pay the $80,000+ tax bill without selling appreciated investments (which triggers more taxes).

- In retirement, living in Florida, her tax rate on withdrawals will likely be 22–24% federal, and zero state. That’s 15+ percentage points lower than today.

- Because she plans to give a lot to charity, those Traditional IRA dollars can be donated directly to charity in retirement at a 0% tax cost.

The better plan:

Wait until she retires at 67. Then she’ll have a window before age 75, living in Florida, with no salary, to convert at much lower rates. The dollars she would have converted today at 42% all-in will instead convert at about 22%. On a $200,000 conversion, that’s roughly $40,000 in tax savings, every single year she chooses to convert.

Why this doesn’t work:

Peak earning years + high-tax state + no outside cash for taxes + charitable plans + upcoming move to a tax-free state = wait.

Case Study 3: Mark & Jenna – The Middle Ground

Both 58. Semi-retired. Living in North Carolina.

| Traditional IRA / 401(k) | $1.1 million combined |

| Roth IRAs (already) | $180,000 |

| Brokerage account | $220,000 |

| Mark’s consulting income | $65,000/year |

| Jenna’s income | $0 (just stopped working) |

| Health insurance | Marketplace plan with subsidies (until 65) |

Why this one is harder:

Mark and Jenna aren’t the clear “yes” of Tom and Linda, but they’re also not the clear “no” of Dr. Patel. They’re in the gray zone, which is where most real people sit.

Mark’s consulting income already uses up part of their 12% tax bracket, so they can’t convert a huge amount cheaply. They have a 9-year runway before Jenna’s Social Security starts. They have cash to pay the tax. But they’re also on a Marketplace health plan with subsidies that could disappear if their income gets too high.

The move:

Convert a modest amount, about $60,000 this year. That fills most of the remaining 12% bracket without crossing into 22%. The all-in tax cost (federal + North Carolina) is about $9,750, or roughly 16% blended.

But there’s a catch we have to model first: ACA health insurance subsidies. If $60K of extra income costs them $15,000 in lost subsidies, the true cost of that conversion jumps from 16% to over 40%, and the move stops making sense. So we run the ACA calculator before pulling the trigger.

If subsidies aren’t a factor (they’re on employer COBRA or a non-subsidized plan), we go ahead. If they are, we either wait, convert less, or coordinate around it.

The multi-year plan:

| Ages | What’s happening | Convert |

| 58–64 | Mark still consulting; fill up the 12% bracket each year | $50–70K/yr |

| 65–66 | Medicare starts; ACA worry gone; can push higher | $100–150K/yr |

| 67–69 | Jenna’s Social Security kicks in; less room | $40–70K/yr |

| 70+ | Mark’s Social Security starts; RMDs at 75 | Minimal |

Over 12 years, this approach moves roughly $500,000–$700,000 to the Roth side, leaving some money in the Traditional IRA for charitable giving and lower-bracket years later.

Why this needs careful planning:

Modest current income + ACA subsidies in play + state tax + long runway = small conversions now, larger later. Most clients look more like this than the textbook cases.

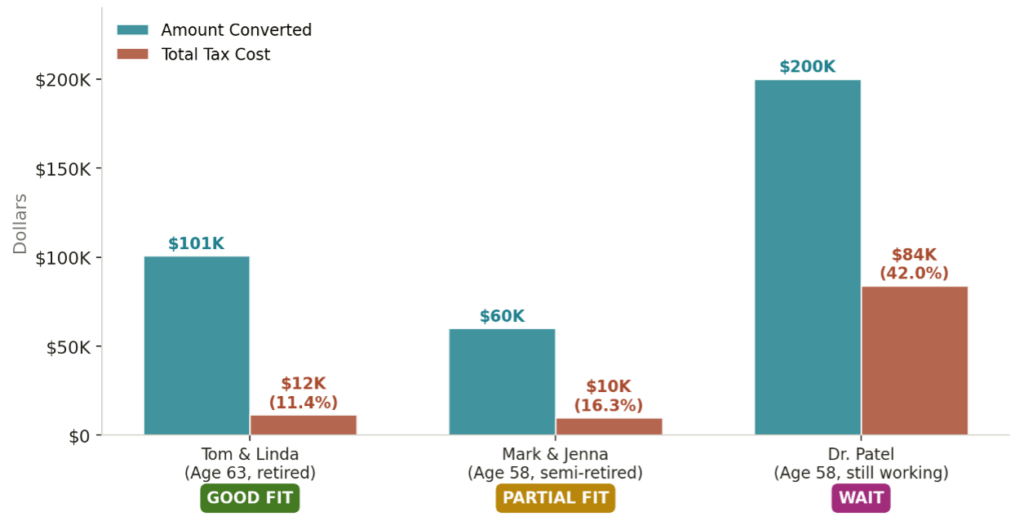

All Three Side-by-Side

The chart below shows what each couple converts, what it costs them, and the verdict for each:

The Bottom Line

Roth conversions aren’t a one-size-fits-all move. They’re a multi-year strategy that has to be coordinated with your full financial picture: your income, your retirement timing, your state of residence, your health insurance, your charitable plans, and your kids’ eventual tax situation.

The clients who benefit most usually have three things in common:

- A temporary low-income window (often the early retirement years before Social Security and RMDs).

- Cash outside the IRA to cover the tax bill.

- A long runway for the money to grow tax-free.

The clients who should usually wait are still working at high incomes, don’t have outside cash to pay the tax, or plan to move to a lower-tax state.

If you’re not sure which group you’re in, our advisory team can help. We’ll model your specific situation, including the moving parts most people overlook, and figure out the right move, the right amount, and the right timing.

Sources

The following sources informed the tax figures, thresholds, and regulatory references used throughout this article:

1. Northern Trust “Roth IRA Conversions Under the OBBBA”

2. The Reed Corporation “2026 Tax Brackets”

3. Income Lab “Roth Conversion Strategy: 2026 Guide”

4. Bankers Life “The Roth IRA 5-Year Rule: What It Is and How Does It Work”

5. CNBC “Tax Brackets and Standard Deductions 2026”

The information contained in this article is provided for general educational and informational purposes only. It is not intended to be, and should not be construed as, personalized investment advice. No portion of this content should be interpreted as a recommendation to buy, sell, or hold any security, to engage in any investment strategy, or to execute a Roth conversion or any other tax-related transaction. Roth conversions involve complex tax, financial, and estate planning considerations that vary significantly based on individual circumstances. The case studies presented are hypothetical illustrations created solely to demonstrate general planning concepts. The individuals depicted are not actual clients of Alliance Wealth Advisors, LLC, and the facts, figures, account balances, tax outcomes, and projections are illustrative only. Your results will differ based on your specific tax situation, income, state of residence, account types, health status, family situation, market performance, and applicable laws at the time of any transaction. Tax laws are complex and subject to change. References to federal tax brackets, IRMAA thresholds, Required Minimum Distribution (RMD) ages, Affordable Care Act subsidies, state income tax treatment, the One Big Beautiful Bill Act (OBBBA), the SECURE Act, and any other tax provisions reflect our understanding of the law as of the publication date and may not reflect subsequent legislative, regulatory, or judicial changes. Alliance Wealth Advisors, LLC does not provide tax or legal advice. You should consult a qualified tax professional, CPA, or attorney regarding your specific situation before implementing any strategy discussed in this article. Any projections, illustrations, or forward looking statements, including assumed growth rates, future tax bracket positioning, RMD projections, and conversion savings estimates are hypothetical, are based on assumptions that may not materialize, and are not guarantees of future results. Actual results may vary materially. Investment returns and account balances will fluctuate, and conversions made today cannot be reversed under current law (recharacterization of Roth conversions was eliminated by the Tax Cuts and Jobs Act of 2017). All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Diversification and asset allocation do not guarantee a profit or protect against loss. Certain information contained herein may be derived from third-party sources believed to be reliable; however, Alliance Wealth does not guarantee the accuracy, completeness, or timeliness of any such information. Reading this article does not create an advisory relationship between you and Alliance Wealth Advisors, LLC. An advisory relationship is established only through a written investment advisory agreement.